# orthog = FALSE gives GIRF.

psGIRF <- function(x, n.ahead = 20, cumulative = TRUE, orthog = FALSE){

y.names <- colnames(x$y)

impulse <- y.names

response <- y.names

# Ensure n.ahead is an integer

n.ahead <- abs(as.integer(n.ahead))

# Create arrays to hold calculations

# [1:nlags, 1:nvariables, shocked variable ]

IRF_o = array(data = 0, dim = c(n.ahead,x$K,x$K),

dimnames = list(NULL,y.names,y.names))

IRF_g = array(data = 0, dim = c(n.ahead,x$K,x$K),

dimnames = list(NULL,y.names,y.names))

IRF_g1 = array(data = 0, dim = c(n.ahead,x$K,x$K))

# Estimation of orthogonalised and generalised IRFs

SpecMA <- Phi(x, n.ahead)

params <- ncol(x$datamat[, -c(1:x$K)])

sigma.u <- crossprod(resid(x))/(x$obs - params)

P <- t(chol(sigma.u))

sig_jj <- diag(sigma.u)

for (jj in 1:x$K){

indx_ <- matrix(0,x$K,1)

indx_[jj,1] <- 1

for (kk in 1:n.ahead){ #kk counts the lag

IRF_o[kk, ,jj] <- SpecMA[, ,kk]%*%P%*%indx_ # Peseran-Shin eqn 7 (OIRF)

IRF_g1[kk, ,jj] <- SpecMA[, ,kk]%*%sigma.u%*%indx_

IRF_g[kk, ,jj] <- sig_jj[jj]^(-0.5)*IRF_g1[kk, ,jj] # Peseran-Shin eqn 10 (GIRF)

}

}

if(orthog==TRUE){

irf <- IRF_o

} else if(orthog==FALSE) {

irf <- IRF_g

} else {

stop("\nError! Orthogonalised or generalised IRF?\n")

}

idx <- length(impulse)

irs <- list()

for (ii in 1:idx) {

irs[[ii]] <- matrix(irf[1:(n.ahead), response, impulse[ii]], nrow = n.ahead)

colnames(irs[[ii]]) <- response

if (cumulative) {

if (length(response) > 1)

irs[[ii]] <- apply(irs[[ii]], 2, cumsum)

if (length(response) == 1) {

tmp <- matrix(cumsum(irs[[ii]]))

colnames(tmp) <- response

irs[[ii]] <- tmp

}

}

}

names(irs) <- impulse

result <- irs

return(result)

}Generalised impulse response function in R.

R

Econometrics

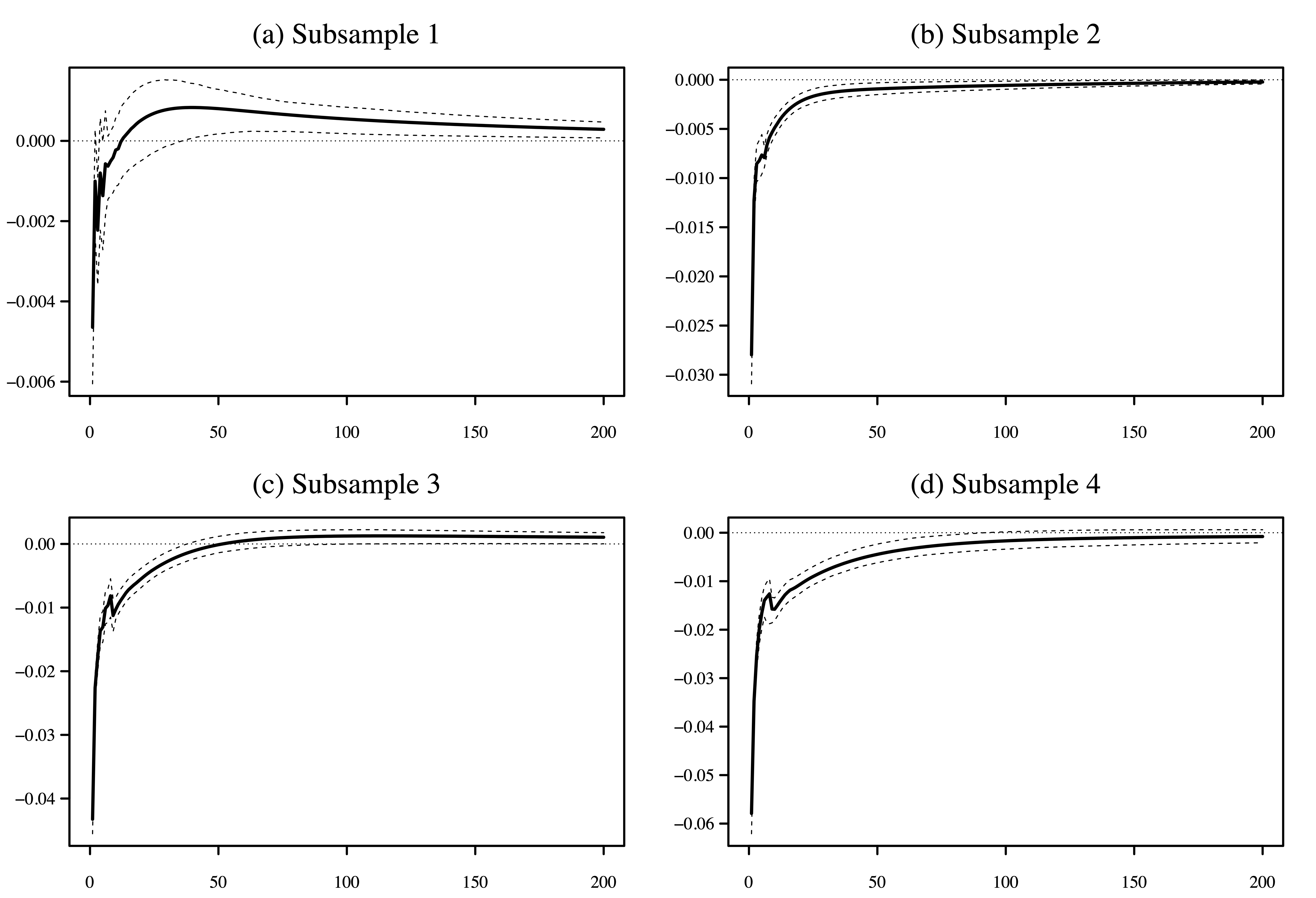

R code for creating generalised impulse response functions (GIRF) from VARS package outputs.

This function is a replacement for the vars package irf function, , that estimates Pesaran and Shin (1998) orthogonalised and generalised IRFs and is intended to be slotted into the vars package boot function, , to bootstrap confidence intervals for IRFs.

I referred to the Matlab code posted by Ken Nyholm.