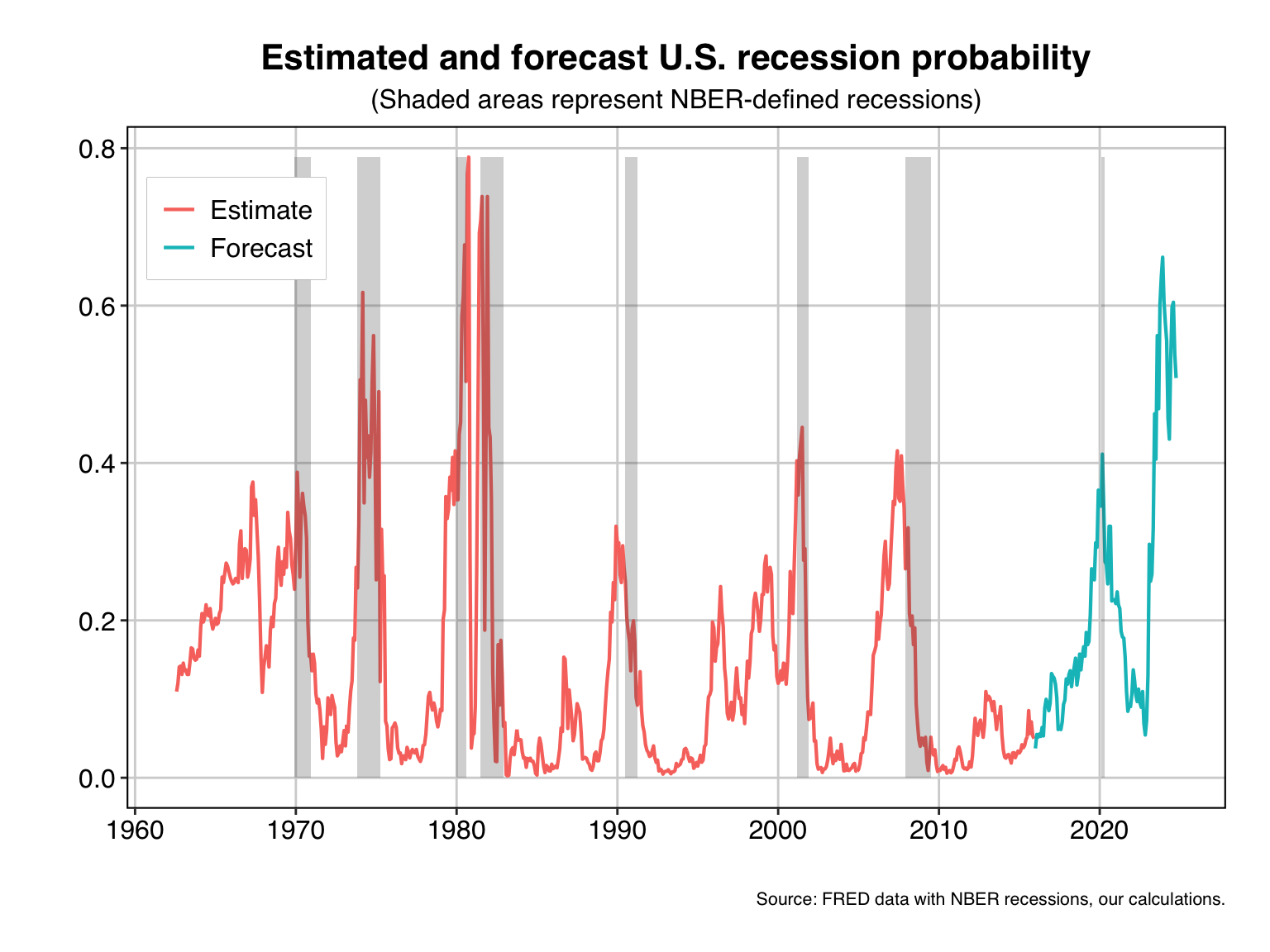

A note on extracting information about future reessions from the term structure of interest rates including R code and analysis of US data.

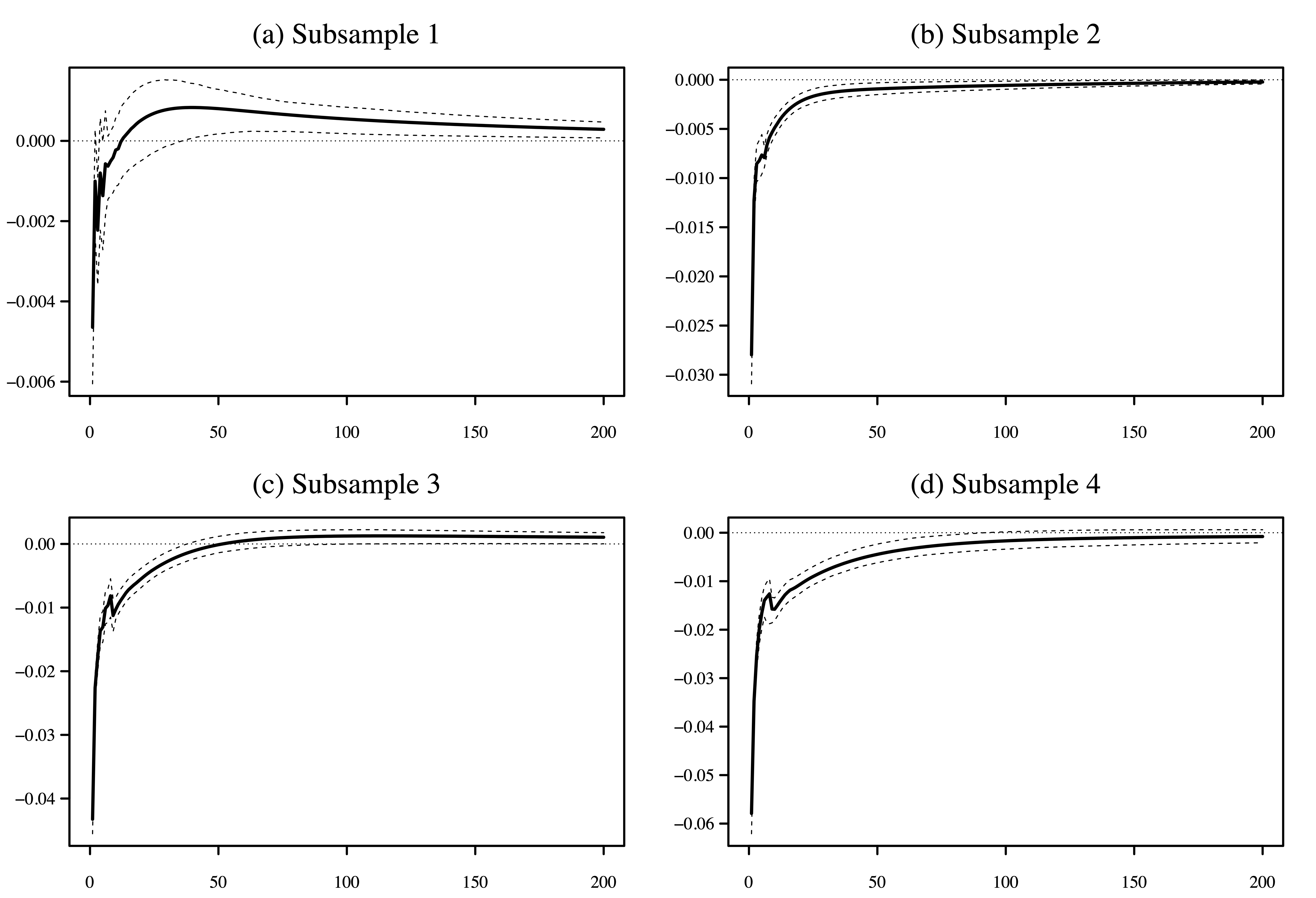

R code for creating generalised impulse response functions (GIRF) from VARS package outputs.

Summary of our commodity market microstructure research on the Japan Exchange Group website.

Summary of our intraday commodity seasonality research on the Japan Exchange Group website.

My co-author Michael McAleer was interviewed in connection with our article on university rankings.